A “Miner” Change to the Government 457(b) May Make a Major Difference To Teachers

A “Miner” Change to the Government 457(b) May Make a Major Difference To Teachers

The one constant in the defined contribution world is change. For once, Congress may have made a change that could unintentionally alter the course of teacher supplemental retirement plans.

Up until the end of 2019, there was one big difference between the 403(b) and the 457(b) that tended to favor contributing to a 403(b) over a 457(b). Thanks to a law passed at the end of 2019, that major difference is now gone and contributing to a 457(b) before a 403(b) could make more sense. In fact, it could completely change the defined contribution plan landscape for public school employees going forward.

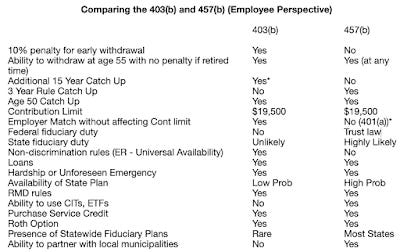

A 457(b) is a little known plan that is similar to the 403(b) and generally the primary defined contribution option offered to state and municipal employees. The 457(b) has been available to teachers as well, but has largely been ignored in favor of the 403(b). Both plans have similar contribution limits and the ability to contribute on a pre-tax and Roth basis. The one major difference was that money contributed to a 457(b) is never subject to a 10% federal penalty if withdrawn prior to age 59 1/2 (with a few exceptions including the fact you must separate from service). A minor, but meaningful difference was that 457(b) money cannot be accessed prior to a teacher separating from service completely (meaning not just retirement, but also for subbing). 403(b) plans grant access to money without penalty at 59 1/2 regardless of employment status. This is a big advantage for teachers who plan on working past age 60. This access to money difference is what is changing and it’s due to a struggling coal miner pension fund.

The United Mine Workers of America health and pension funds, like more than 1,400 similar one-industry plans, were underfunded. Then along came The American Miners Act of 2019. This new law will help stabilize the private multi-employer pension, but it could also inadvertently nudge teachers away from the 403(b) and towards the 457(b). Let me explain…

Congress requires expenditures for new laws to be “paid for” and one way of raising money for the coal miners pension fund was to accelerate taxes on 457(b) money. Included in the new act, is a provision that allows in-service 457(b) withdrawals at age 59 1/2 leveling the playing field with the 403(b) on access.

Currently, the favored defined contribution plan for teachers is the 403(b). But because the K-12 403(b) is not subject to ERISA fiduciary oversight, most plans feature high-cost products sold by high-commission sales agents. The New York Times and The Wall Street Journal have documented these issues. My pod partner and owner of 403bwise.org, Dan Otter, touched on the ERISA issue in a recent blog post.

By design, the 457(b) requires more fiduciary oversight which has generally led to better, lower cost investment options. It now might make more sense for teachers to contribute to the 457(b) before contributing to a 403(b). Teachers are allowed to contribute the maximum permittable to both plans. I still love the 403(b) and will continue to advocate for better 403(b) plans, but it might be time for employers (and employees) to begin favoring the 457(b) over the 403(b).

The biggest advantage of the 403(b): Ability for ER contributions*The biggest disadvantage of 403(b): Embedded multi-vendor system, no fiduciary

The biggest advantage of the 457(b): No 10% penalty, everThe biggest disadvantage of 457(b): Odd Salary Reduction rule (month prior)

The agent in the lobby or lunch room isn’t going to tell you about the 457(b) because they normally don’t get paid to do so. They might even actively try to get you to invest in the 403(b) over the 457(b).

There is one caveat, not all 457(b)s are worthy. You still need to do due diligence. In California there are two great state based 457(b) plans, CalSTRS Pension2 and CalPERS 457. Yet most school districts fail to offer either, opting instead to offer substantially lower quality 457(b) plans that pay revenue to their compliance administrator, insurance agents or both. Just like with the K-12 403(b), teachers may have to lobby their school district to get a better plan.

*Technically 457(b) can have employer contributions, but they count toward the employee contribution limit. This can be overcome by adding a 401(a) plan.

Miners Act of 2019

With help and edited by Dan Otter of www.403bwise.org