Don't Fall For This 403(b) "Match" Scam

Several private universities are being sued for overcharging participants, the companies offered were low-cost providers like TIAA, Fidelity and Vanguard...yet they are still being sued.

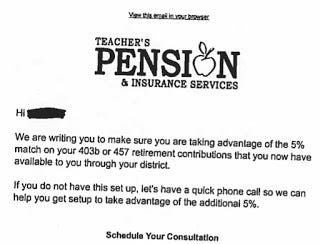

Meanwhile, in the public K-12 market we have companies like the one featured in the ad to the left literally lying to participants and potential participants about being eligible for an employer match. They represent companies like Midland National and Life of the Southwest, companies that are not in participants best interest.

I feel like I'm in the Twilight Zone. They don't call the public K-12 market the Wild West for nothing (I wrote a book for advisors titled "Wild West: Providing Fiduciary Advice to Public School Employees").

If you are a teacher and you receive the e-mail featured above, would you not think that your school district is offering a match of 5% if you begin contributing to your employer's 403(b)? I know that's how I would read it if I weren't in the financial services business.

Lucky for you, I am in the biz and can help you decipher this scam.

First, it's extremely unlikely the school district is offering any match and it's also unlikely they have endorsed or authorized the company featured to send the e-mail (if they did, they are opening themselves to significant liability). What is really going on?

It's actually pretty simple, this is an insurance agent using (in my opinion) underhanded and dishonest methods to lure unsuspecting teachers into buying high commission, retail annuity products that are likely better for the agent selling them than they are for the actual purchaser.

The participant doesn't actually get a "match", instead they get a "bonus" paid by the insurance company for every dollar placed in the annuity product. This "bonus" doesn't come for free, you pay for it in one way or another. One way a participant might pay for the bonus is through a longer surrender period on contributions, many annuity companies will add five years to the policy's surrender period and increase the surrender charge. This allows the annuity company to keep your money longer and make up for paying the bonus by underpaying interest for an additional number of years. Another way of paying for the cost of the bonus is to pull the strings of the policy to manipulate the rate paid so that it is lower than a comparable policy.

There is no free lunch, an annuity company is NOT going to give you free money. Every dollar they "give" you will be taken away in some form or fashion.

If you receive an advertisement similar to the one above you should ignore it. Better yet forward it to the state insurance commission.

Scott Dauenhauer, CFP, MPAS, AIF

Hat Tip to Don St. Clair for sending me the e-mail.Are you 403(b) Wise? 403bwise.org is the place on the internet to learn, advocate and build community.