How Is This Still A Thing? Annuity Ads

John Oliver has a segment on his HBO show Last Week Tonight named “How is This Still a Thing?” and lately I’ve been scratching my head wondering the same thing about annuity advertisements.

8% Annuity Returns? Hmmm…curious.

I received an e-mail from this company (above) the other day advertising “Annuity Returns” of 8%+. If you are a consumer and you see such a high interest rate compared to what the rest of the world is paying ($7 Trillion in assets globally currently trading at negative rates) are you not likely to click to investigate further? Who wouldn’t.

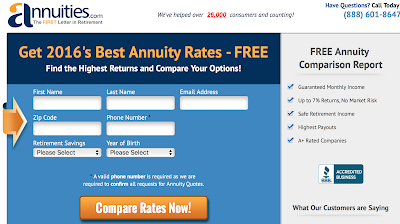

7% Returns with “No Market Risk”…Wow!

Here is another one sent to me by a client who wondered why we were “only earning 3% for our fixed income?”. A good question if 7% interest rates are available, why am I only able to get less than half? You’ll notice that this website is even a Better Business Bureau Accredited Business. Is it reasonable to assume that one could earn 7 or 8% from an annuity without any market risk? Not at this point in time. Let me explain why.

These companies are advertising fixed annuities, even though the returns advertised seem like what one might get from an aggressively invested variable annuity. There is no possible way a fixed annuity can deliver a steady 7 or 8% return in today’s market environment.

Bloomberg recently pointed out that nearly $7 Trillion dollars in global bonds are now yielding a negative rate. Rates in the United States are actually high compared to many parts of the world, though they’ve recently been falling again.

Insurance companies are limited in what they can invest their General account in (the General account is where your money goes when you hand your money to an insurance company in exchange for an annuity contract) due to current insurance regulations. General accounts are not going to be heavily invested in stocks and while they can hold risky assets, they are generally (no pun intended) invested in higher quality fixed income (as well as some real estate and other risky assets, but only in smaller portions).

High quality fixed income is not yielding much these days. Even if we assume that an insurance company could earn a rate of 5% on new money invested in the General Account (a stretch in my opinion), they would need to pay you much less to account for client acquistion costs (commissions to sales agents), servicing and profit to shareholders. The company might pay out 3%, keeping the difference for the costs I just outlined. 3% is a far cry from 7% or 8%.

If you look closely you will not find many annuities paying 3% right now, most pay well below that. The portfolio that an insurance company would need to support a 7 or 8% payout is simply not allowed be held and even if it where, it’s unlikley the payout could be maintained at such high levels.

So what’s really going on here?

False and Misleading Advertising, in my opinion.

These sites are likely trying to lure unsuspecting savers into the clutches of their sales agents so that they can likely be sold a commissionable fixed annuity product called an Equity Indexed Annuity (sometimes called a Fixed Indexed Annuity).

Equity Index Annuities (EIAs) are fixed annuity products that have an interest rate linked to a market index, but are not invested in the market index. They are very complicated and can occasionally have a payout in a single year that is in the 7% or 8% range, sometimes even higher. The catch is that they will also give you no interest in years where the market linked index is down.

EIA’s in theory should pay out a higher interest rate over time than a fixed annuity of the same maturity due to the fact they are higher risk (years where you can be credited zero interest), though I’m not aware of any study that has demonstrated this to be true. In reality, the higher commissions paid out on these products may actually reduce the return below that of a normal fixed annuity (again, I have no evidence for either claim…as neither have been studied, rather studied publicly, the insurance companies know).

EIAs are highly profitable for insurance companies.

These advertisements are in my opinion blatantly misleading. They are advertising a rate that cannot be captured by investors as a reality. I’m unclear how this practice is allowed, it’s another example of poor regulation in the insurance industry and why a national regulator needs to be created. Bottomline, if something seems to good to be true, 99% of the time it will be. You cannot get a 7% return from a fixed annuity on a regular basis. Don’t click on these ads, they are simply trying to connect you to a sales agent trying to sell you a product unlikely to be in your best interest.

Scott Dauenhauer, CFP, MPAS, AIF